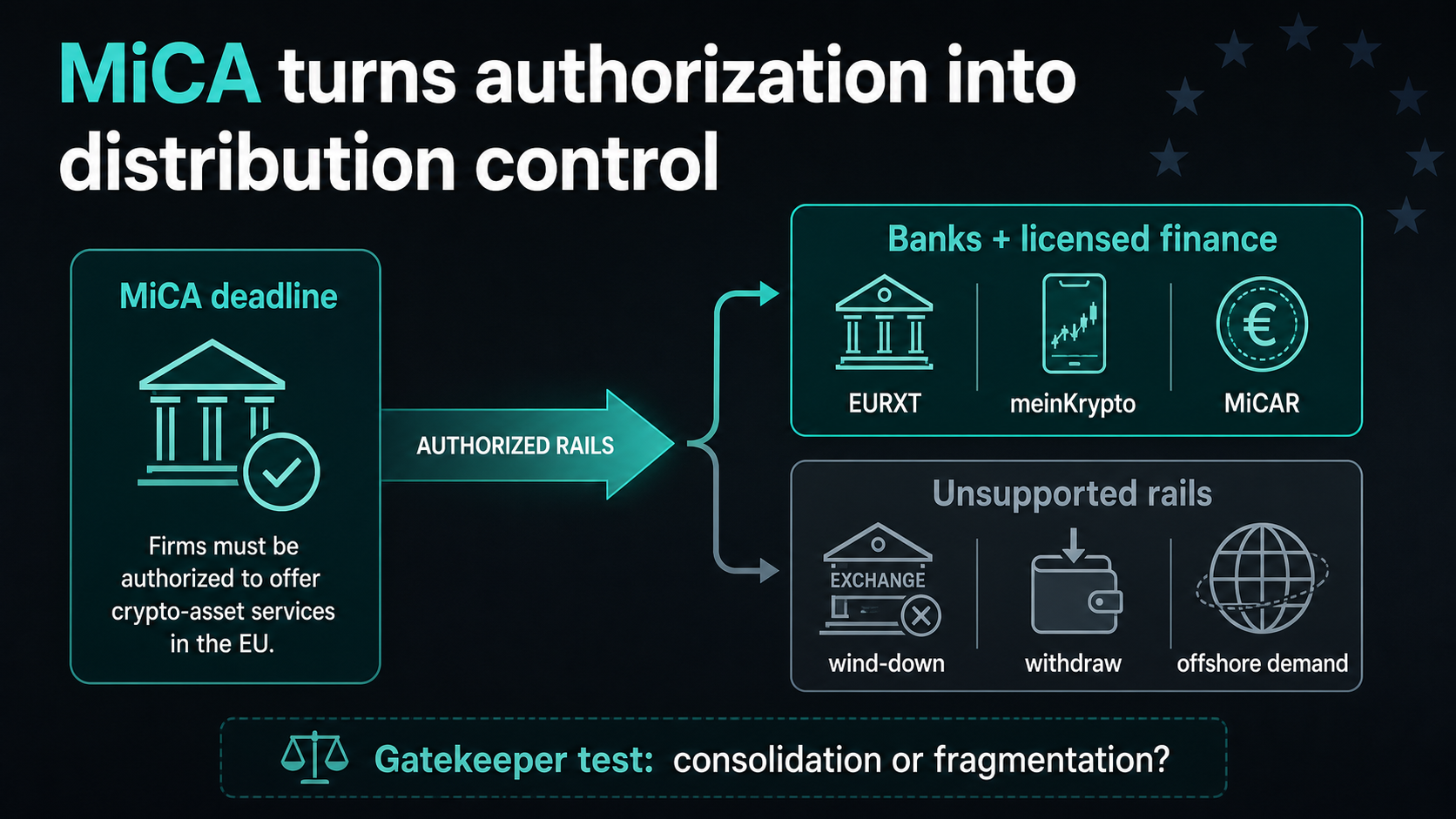

Europe’s MiCA deadline has now entered the phase in which licenses begin to shape distribution.

The first wave of concern centered on which platforms European users could still reach after July 1. The next phase is more structural. MiCA is deciding which issuers, banks, asset servicers, and app providers can continue offering stablecoins and crypto products to customers within the regulated market.

ESMA says MiCA creates uniform EU rules for crypto-asset issuers and service providers, covering transparency, disclosure, authorization and supervision. Its interim MiCA register was last updated on July 3, two days after the transitional period for many existing crypto-asset service providers expired.

That timing matters because the end of the grandfathering period changes MiCA from a licensing deadline into a distribution filter. Authorized firms can keep serving the market. Unauthorized firms must move toward exit, transfer, or closure.

ESMA’s June 23 statement told unauthorized crypto-asset service providers to stop onboarding new EU clients, stop opening new client relationships or accounts, cease marketing and solicitation, and limit activity to steps needed to sell, transfer, reallocate or close positions. Custody can continue only for the strictly necessary period for an orderly exit.

That is the regulatory frame. The market effect is sharper: MiCA is turning authorization into a source of distribution power.

Banks are moving into the gap

The clearest example comes from within traditional finance.

CACEIS said Crédit Agricole launched EURXT on July 1 as a euro-denominated electronic money token issued on Ethereum by CACEIS. The group described it as MiCA-compliant, pegged to the euro, backed one-to-one by fiat euros and initially available to institutional investors and corporate clients of CACEIS.

The first use case was settlement for a subscription into a tokenized Amundi money market fund rather than a consumer wallet campaign. That detail shows where compliant stablecoins may first gain traction in Europe: inside asset servicing, fund settlement and bank-controlled institutional workflows.

CACEIS also said EURXT’s reserves are made exclusively of cash held on the balance sheet of CACEIS Bank. The token’s compliance pitch is therefore more than Ethereum issuance. The reserve, issuer, and client channels all sit within a regulated financial group.

That structure matters because stablecoin competition in Europe may increasingly depend on who can combine on-chain settlement with a regulated balance sheet, a trusted client base and a distribution channel that supervisors already understand. A euro token issued through an asset servicer enters the market with a different path from an offshore dollar stablecoin seeking placement on crypto-native venues.

Germany’s cooperative banking sector is building the other side of the same map.

DZ Bank said it received BaFin MiCAR authorization at the end of December 2025 for meinKrypto, a wallet and trading service that will be integrated into the VR Banking App. Participating Volksbanken and Raiffeisenbanken still need to obtain their own BaFin notification and implement it before offering it, but once they complete those steps, customers can invest in crypto fully digitally through the banking app.

The launch set includes Bitcoin, Ethereum, Litecoin and Cardano. DZ Bank also cited a September 2025 Genoverband study, which said more than one-third of cooperative banks planned to introduce the crypto solution in the following months.

CryptoSlate’s Ethereum page listed ETH at about $1,763.10 on July 5, while CACEIS’ use of Ethereum shows how public-chain settlement can still be routed through bank-issued instruments.

That is a distribution story. A self-directed customer can access crypto through the banking app they already use, rather than searching for a separate platform. If enough cooperative banks implement the service, MiCA-compliant access becomes part of ordinary account infrastructure.

USDT shows the other side of the filter

The bank rollout is happening as dollar-stablecoin access faces more platform-by-platform risk in Europe.

WuBlockchain reported on X on July 4 that Revolut is phasing out USDT support for European users. The reported timetable says users can buy USDT until July 6; new deposits stop on July 30; selling or withdrawing to external wallets remains available until August 31; and remaining balances are converted to fiat after that date.

The delisting fits the broader MiCA pattern: platforms must decide whether supporting a token, an issuer, or a service creates excessive regulatory exposure after the deadline.

MiCA addresses authorization and compliance risks rather than directly prohibiting USDT. If a large retail app decides that a token no longer fits its European compliance path, the practical result for users can resemble a loss of access, even when the legal mechanism is licensing and platform risk management.

The stakes are large because USDT is market infrastructure. CryptoSlate’s Tether page listed USDT at about $184.11 billion in market value and $45.56 billion in 24-hour volume on July 5. It is one of crypto’s main dollar settlement and trading rails.

The broader CryptoSlate coin rankings showed a $2.17 trillion crypto market and $52.38 billion in 24-hour volume yesterday, July 5, with USDT ranking third by market capitalization behind Bitcoin and Ethereum.

That scale is why the post-deadline question reaches beyond one fintech and one token. Europe is testing whether regulated venues can make compliant euro-denominated instruments useful enough to compete with the liquidity habits built around USDT. If they can, MiCA redirects stablecoin access toward issuers and distributors inside the bloc. If they cannot, users may keep searching for dollar liquidity outside the supervised perimeter.

The difference between those outcomes will show up in venue support, app availability, wallet flows and settlement use cases rather than in a single legal announcement. Every platform decision becomes another signal about where stablecoin demand is being routed.

The moat is compliance plus distribution

MiCA was written as a harmonized rulebook for investor protection, market integrity and financial stability. Those aims matter, especially for users who were exposed to platforms operating under uneven national regimes.

But regulation also changes market structure. After July 1, a compliant issuer or bank holds more than a license. It has a channel that competitors cannot match within the EU without authorization.

Crédit Agricole and CACEIS can place a euro stablecoin in tokenized fund settlement. DZ Bank can embed crypto trading inside the cooperative banking network’s app infrastructure. Licensed exchanges and brokers can absorb users leaving non-compliant platforms. Meanwhile, products outside the MiCA perimeter depend on offshore access, self-custody, or platforms willing to absorb the compliance risk.

That is the gatekeeper effect. It is less dramatic than a sudden prohibition, but it may be more durable. Distribution in finance often belongs to whoever owns the trusted account, the settlement workflow, and the customer relationship. MiCA is making those advantages more valuable in crypto.

The result could be cleaner, safer access for users who move to authorized rails. It could also give large banks, asset servicers and licensed finance groups a structural advantage over crypto-native firms that struggle to secure approval, maintain local compliance teams or preserve token coverage under the new rules.

CryptoSlate has already covered the first-order MiCA questions: Binance and USDT liquidity, and the user-migration test created by the July 1 deadline. The next test is who benefits after those migrations happen.

One path is clean consolidation. Compliant banks, asset servicers, and licensed exchanges absorb more activity, euro-denominated EMTs gain wider use in real settlement, and users get clearer protections.

The other path is fragmentation. Users keep chasing USDT liquidity outside licensed European rails, offshore platforms keep serving demand from beyond the perimeter, and the EU gains a cleaner rulebook without capturing the flows it most wants to supervise.

The answer to whether MiCA makes banks the next stablecoin gatekeepers is therefore conditional but strong. The law does not hand banks control by itself. It makes authorization, custody, reserve structure and app distribution the gates through which compliant crypto access now has to pass.

In the first week after the deadline, those gates are already looking more like bank doors.