Bitcoin treasury preferred stocks are moving from a simple income story into a credit test on Bitcoin balance sheets.

Strategy remains the center of gravity, but Strive, the 7th largest public Bitcoin holder, has now put the spillover in public numbers: another Bitcoin treasury company held a Strategy preferred stock and watched that position become a market signal of stress.

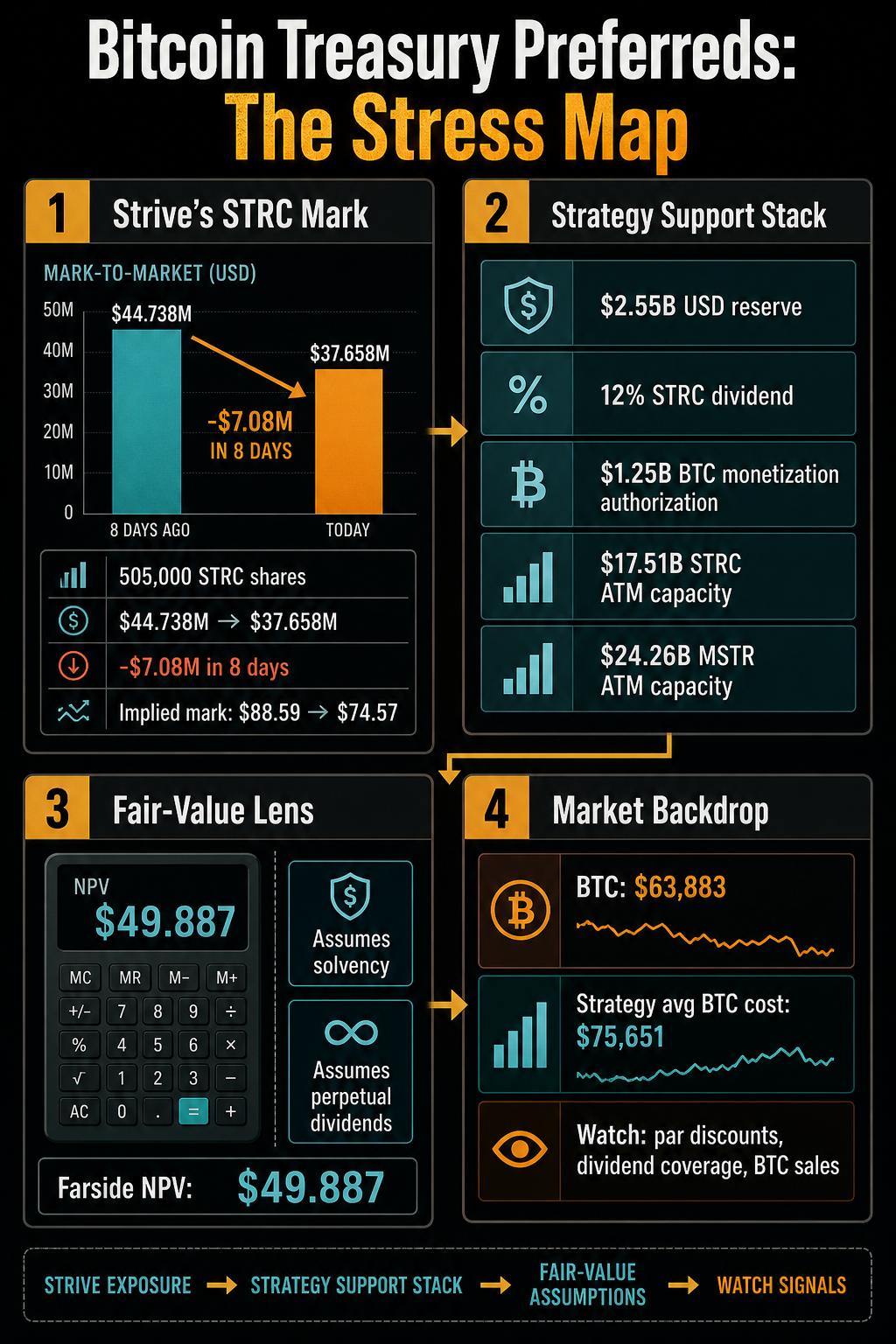

In its June 29 update, Strive disclosed that it held the same 505,000 STRC shares on June 18 and June 26, while the fair value of that position fell from $44.738 million to $37.658 million.

That $7.08 million change happened without a disclosed change in the STRC share count. On a simple division of the filed fair-value figures, Strive’s implied mark moved from roughly $88.59 per share to $74.57 per share in eight days.

The disclosure stops short of proving insolvency, forced selling, or a broken capital model. It shows something more specific. Stress on a Bitcoin treasury preferred stock can ripple through another company’s balance sheet before any dramatic failure occurs.

Strive still reported 19,864 BTC held, cash and equivalents of $141.7 million as of June 26, and 7,829,502 shares outstanding of its own SATA preferred stock. The stronger signal is the way its disclosed Strategy-preferred exposure changes how investors read the category.

The strongest indicator is the way its disclosed Strategy-preferred exposure changes how investors read the category.

The public question around Strategy’s STRC has been whether investors are still treating the instrument as an income product or as stressed credit linked to Bitcoin, market liquidity, and Strategy’s ability to support the dividend. Strive’s disclosure makes that question bigger.

A Bitcoin treasury company holding another Bitcoin treasury company’s preferred stock creates a visible cross-company channel. If STRC trades at a discount, Strive can show the damage in its own reported fair value. If SATA then comes under similar scrutiny, the market has a way to compare whether stress is isolated or spreading across the preferred-stock funding model.

Preferred-stock treasury products are sold around yield, stated amount, and recurring payments. That makes them look familiar to income investors. Once the central questions become discount to par, reserve coverage, dividend resets, repurchases, and possible asset sales, the instrument starts trading like credit.

The investor is now asking whether the issuer has sufficient cash support, market access, and Bitcoin liquidity to maintain the credibility of that coupon.

Strategy’s New Playbook Looks Like Credit Management

Strategy’s own June 29 filing reinforces that shift. The company announced a Digital Credit Capital Framework comprising a USD reserve policy, a revised STRC dividend policy, preferred-security repurchases, common-stock repurchases, and a BTC monetization program. Those are management tools for a capital structure under market pressure.

Strategy said its USD Reserve stood at $2.55 billion as of June 28 and that management must maintain at least 12 months of expected annual preferred-stock dividend payments and interest obligations unless the board authorizes a lower level. The same filing said that reserve can be replenished through BTC sales under the monetization program or through other capital-market activity.

That reserve is important because Strategy also raised the STRC regular dividend rate to 12.00% per year, payable semi-monthly, with record dates on or after July 1. Strategy said it declared $ 0.50-per-share cash dividends for the periods ending July 31 and Aug. 15, subject to the conditions in STRC’s certificate of designation.

A higher dividend can support an income instrument, but it also raises the question of how durable the payment is if the security remains discounted.

Strategy made that feedback loop explicit. Its STRC dividend policy will consider STRC trading levels, market yields, credit spreads, Bitcoin price and volatility, reserve coverage, capital-market conditions, and the company’s overall capital structure. The filing also said STRC dividends are not guaranteed and will not necessarily rise solely because STRC trades below its stated amount.

That is the language of active credit management. Strategy also authorized up to $1.0 billion in repurchases of its Digital Credit Securities, with STRC expected to be the initial priority if management deems repurchases accretive and supportive of the capital structure. It authorized another $1.0 billion for Class A common-stock repurchases. Those authorizations do not require the company to buy securities, but they show the range of tools management may use if discounts become too damaging.

The same framework makes BTC sales part of the discussion. Strategy’s board authorized a BTC monetization program that can sell Bitcoin to generate up to $1.25 billion for the USD Reserve, help fund or replenish preferred dividends and interest payments when management deems it preferable to issuing common stock or using other capital-market transactions, and fund securities repurchases.

The company was clear that the program does not obligate it to sell Bitcoin. Still, the authorization changes the discussion. A balance sheet built around accumulation now has a formal path for using BTC to defend parts of the credit stack.

The Fair-Value Test Is About Durability

Farside’s public STRC fair value calculator gives one way to see why the debate has moved beyond headline yield. As viewed by CryptoSlate on July 7, the calculator showed an estimated net present value of $49.887 per STRC share under its displayed assumptions, with a dividend schedule starting at an 11.50% coupon and declining to 3.60% from month 33 onward.

Its most important caveat is that the calculation assumes the company remains solvent and pays the dividend in perpetuity.

That is not an official Strategy valuation, and it should not be blended with Strategy’s separate 12.00% STRC dividend disclosure. It is useful because it shows what preferred-stock investors are actually testing. The value is highly sensitive to assumptions about dividend durability, discount rates, and the issuer’s ability to continue paying under varying Bitcoin and capital-market conditions.

The Bitcoin backdrop makes the test harder to dismiss. CryptoSlate Bitcoin market data shows BTC trading around $62,000 on July 8, down 1.8% over 24 hours but up 5.5% over seven days, with a $1.24 trillion market capitalization and 58% dominance.

Yet Strategy’s June 28 BTC update reported 847,363 BTC held at an average purchase price of $75,651. That gap does not force a sale, and Strategy reported no Bitcoin purchases for the June 22-28 period. It does, however, explain why the market is paying attention to reserve policy, ATM issuance, and BTC monetization language.

Strategy’s ATM table shows how much capital-market capacity still sits behind the model. During June 22-28, Strategy reported no preferred-stock ATM sales, 12,669,017 MSTR shares sold, and $1.1524 billion in MSTR net proceeds. It also listed the remaining issuance capacity of $17.5108 billion for STRC and $24.2575 billion for MSTR, as well as other preferred programs.

The model still has tools. The question is what those tools cost when investors demand higher yields, larger discounts, or more visible backstops.

What Would Prove The Stress Is Broader

The market now has two broad ways to read the next phase. The market now has two broad ways to read the next phase. In the contained scenario, STRC discounts tighten, Strategy’s USD reserve and dividend policy calm the market, BTC sales remain optional rather than necessary, and Strive’s mark-down looks like a temporary hit on one cross-holding. That would keep the pressure mostly inside Strategy’s orbit.

In the broader-stress scenario, discounts persist, dividend-rate changes no longer reassure investors, reliance on common-stock ATMs rises, BTC monetization shifts from authorization to use, and Strive’s own SATA preferred starts trading as a comparable stress point rather than a separate product. That would make Bitcoin treasury preferreds a category trade rather than a single-company problem.

The filings do not prove the second scenario has arrived. They do show why the question is being asked. Strive’s STRC position turned Strategy’s discount into another company’s fair-value movement.

Strategy’s framework turned dividends, reserves, repurchases, ATM issuance, and potential BTC sales into a single, cohesive support system. Farside’s calculator showed why solvency and perpetual-payment assumptions matter to preferred value.

The market test is now practical: whether STRC and SATA close or widen their gaps to par, whether dividend coverage looks more credible, whether Strategy leans harder on common-stock issuance or preferred issuance, and whether BTC sales remain only an authorization.

Strive’s next disclosures will help show whether its Strategy exposure was an isolated mark or the first public sign that Bitcoin treasury credit stress is spreading across the preferred-stock model.