Bitcoin is entering the second half of the year with its support system, which powered its last rally, under pressure.

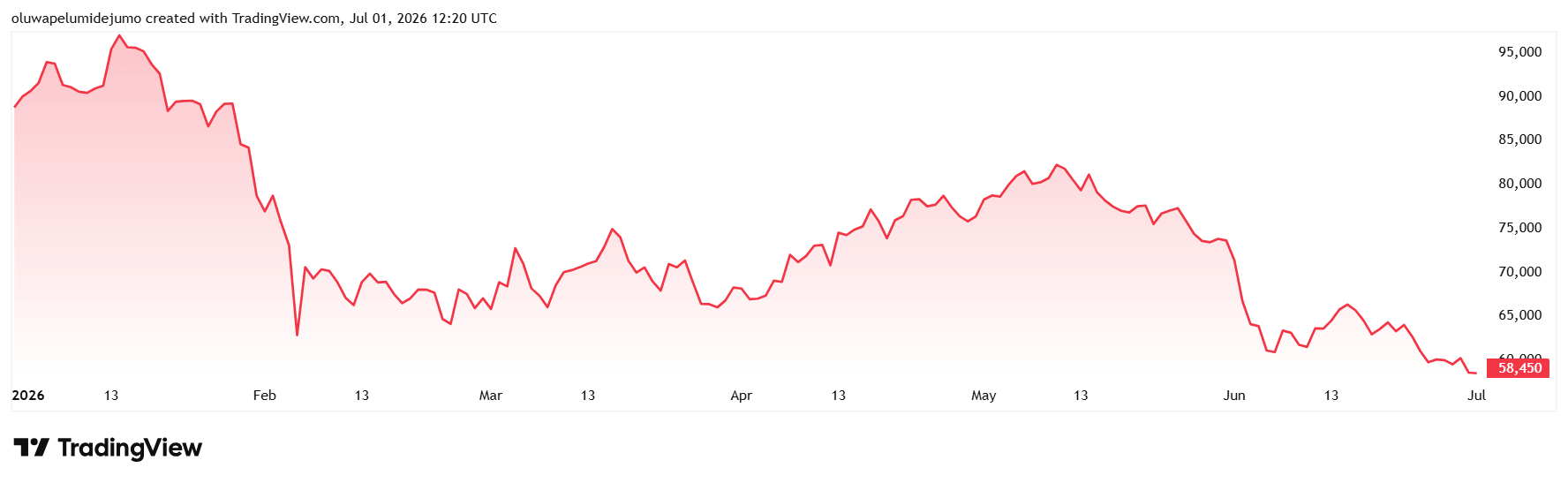

Data from CryptoSlate shows that the largest digital asset has fallen about 33% this year and more than 50% from its October record high above $126,000, trading near its weakest level since September 2024 at around $58,600 as of press time.

This price action has pushed Bitcoin below key long-term trend levels and made the first half of 2026 its worst start to a year since the 2022 crypto crisis.

That makes July a test of whether the market is nearing exhaustion or beginning another leg lower. The next four weeks bring three pressure points: whether exchange-traded fund outflows slow, whether the Federal Reserve signals another rate increase, and whether Congress can move the CLARITY Act before the August recess.

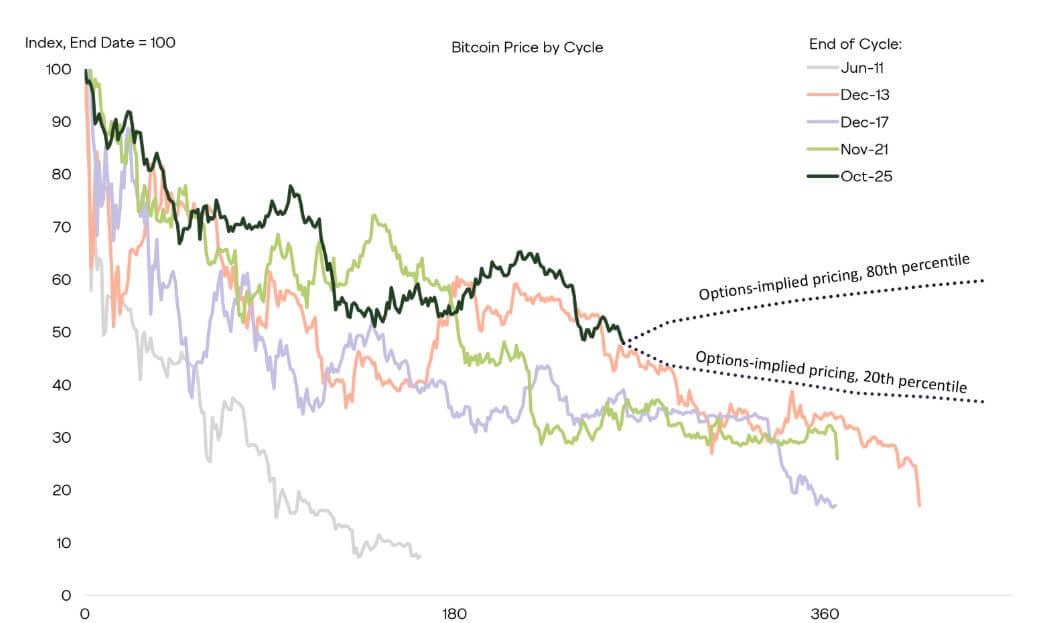

The outcome could determine whether Bitcoin rebounds toward $100,000 by year-end or retests the $50,000 to $55,000 area, which analysts now see as the next major structural support zone.

ETF demand has flipped from cushion to pressure

ETF flows have become one of the clearest signs that Bitcoin’s institutional support is weakening.

Data from SoSoValue show US spot Bitcoin ETFs posted about $4.5 billion in net outflows in June, their worst month since the products began trading in January 2024.

BlackRock’s IBIT accounted for most of the withdrawals, underscoring how the largest regulated demand channel for Bitcoin has become a source of sustained selling pressure.

The weakness was spread across the month rather than concentrated in a single trading session. Spot Bitcoin ETFs recorded only three days of inflows in June, with those positive days totaling less than $100 million combined.

The rest of the month was dominated by redemptions, including several sessions in which hundreds of millions of dollars left the products.

That pressure followed Bitcoin below the $60,000 area and challenged one of the central assumptions behind the ETF-led phase of the market: that regulated funds would provide a steadier base of demand during drawdowns.

Ecoinometrics, a Bitcoin analysis platform, said the decline was consistent with the pressure visible in fund flows, noting that:

“Bitcoin below $60K shouldn’t surprise anyone watching ETF flows. The last 30 days have seen some spectacular days of selling. But they’ve really been defined by relentless selling.”

The firm said nearly every recent trading session had seen capital exit spot Bitcoin ETFs, creating one of the most persistent stretches of outflows since the funds launched. It added:

“That’s the kind of demand shock that keeps pushing prices lower.”

However, the withdrawals do not necessarily point to panic selling.

This is because many ETF investors entered the market at lower prices and may be taking profits or cutting exposure after Bitcoin’s sharp advance last year. But the persistence of the outflows shows that institutional investors are not yet stepping in to absorb the decline.

That marks a clear shift from the earlier stage of the cycle, when ETF demand helped pull Bitcoin deeper into mainstream portfolios and supplied a visible stream of new capital. In June, the same structure showed how quickly large allocators can retreat when prices weaken, macro conditions tighten and momentum fades.

The market is now treating ETF flows as a better gauge of confidence in the top crypto.

So, a return to steady inflows would suggest institutional buyers are willing to rebuild exposure after the drawdown.

But continued redemptions would leave Bitcoin more dependent on long-term holders and less protected by Wall Street demand heading into the second half of the year.

The Fed has removed the rate-cut trade

The ETF retreat is happening just as the rate-cut narrative that carried much of the early-year optimism has broken down.

The Federal Reserve held interest rates steady at its June meeting, but the decision itself was not the market-moving part. The tone was.

Under Chair Kevin Warsh, policymakers have shifted toward a more hawkish stance as inflation remains above target and tariff-related price pressure continues to show up in consumer data.

That has forced traders to reprice the second half of the year. Rate relief, which many crypto investors expected to arrive under a Trump-appointed Fed chair, is no longer the base case. Markets are now considering the possibility that the next move could be a hike rather than a cut.

That shift matters for Bitcoin because the asset does not pay yield.

When Treasury yields rise and the dollar strengthens, investors have less incentive to hold assets whose value depends heavily on liquidity expectations. Bitcoin is absorbing that pressure even as its ETF channel sees redemptions.

The Fed’s change in tone also undercuts one of the market’s earlier assumptions about Warsh. Many crypto investors expected him to lean dovish because President Donald Trump had long pushed for lower rates.

However, that expectation was never as firm as the market treated it. Surveys had suggested only a narrow lean toward dovishness on rates, while many investors expected Warsh to take a tougher stance on the Fed’s balance sheet and preserve some independence from the White House.

The June meeting forced a reset. In March, policymakers were still leaning toward one or two cuts by year-end. By June, the median projection had shifted toward a possible hike, even though the committee remained divided.

That leaves Bitcoin without the macro support many investors expected heading into the summer.

Financial conditions are not easing, the dollar has firmed, and Treasury yields have moved back toward recent highs. For an asset still treated by many allocators as a high-beta liquidity trade, that is a difficult backdrop.

Strategy’s shift raises questions over BTC treasury demand

Meanwhile, market pressure has also spread to the corporate Bitcoin treasury trade, where Strategy’s first sale in years drew attention well beyond the transaction’s size.

Strategy (formerly MicroStrategy) disclosed in May that it sold 32 Bitcoins, worth about $2.5 million. The sale represented only a small fraction of its holdings and did little to alter the company’s overall exposure.

However, the larger concern was the signal it sent to a market that has long viewed Strategy as Bitcoin’s most committed corporate buyer.

For much of the cycle, Strategy stood for a straightforward trade: raise capital, buy Bitcoin and hold through volatility. That made the company an important reference point for investors, especially as spot ETF inflows and corporate treasury purchases reinforced each other.

The sale complicated that view. It suggested Strategy may now be prepared to treat Bitcoin as part of a wider capital-management strategy, rather than as an asset reserved only for accumulation.

The company later reinforced that shift, saying it could sell part of its Bitcoin holdings to strengthen its balance sheet, support its perpetual preferred securities and fund stock repurchases.

The statement gave investors a clearer view of how management could balance Bitcoin exposure against liquidity needs, financing costs and shareholder returns.

Strategy remains closely tied to Bitcoin. Its holdings remain large, and one small sale after years of purchases does not change the market’s supply balance.

Still, the company’s new flexibility has raised a broader question of whether Bitcoin treasury companies will continue to act as steady buyers if prices remain weak and funding conditions tighten.

That question has become more important as Strategy adjusts its financing structure, dividend commitments and reserve policy.

The framework could make the company more resilient by improving liquidity and reducing balance-sheet strain. It also gives management more room to prioritize financial discipline over constant Bitcoin purchases.

For a market already under pressure from ETF outflows, the shift adds another source of uncertainty. Stable corporate holders could help absorb weakness. Slower buying or further deleveraging would remove part of the demand base that supported Bitcoin’s previous advance.

AI is competing for the same risk capital

Despite this current situation, Bitcoin is competing for capital in a market where artificial intelligence has become the preferred risk trade.

Over the past year, hedge funds, asset managers and wealth advisers have poured into AI-linked stocks as investors search for exposure to one of the fastest-growing themes in global markets.

The demand has spilled into new listings, derivatives and exchange-traded products tied to companies seen as beneficiaries of the AI buildout.

That appetite has kept risk-taking alive across parts of Wall Street. But much of the money is moving toward chipmakers, data-center operators, software companies and other firms with a clearer earnings link to AI infrastructure, rather than into crypto.

The split complicates Bitcoin’s market signal. Its decline is not due to investors abandoning risk altogether. Capital is still moving into speculative areas, but Bitcoin is no longer the main destination.

AI offers investors a more immediate corporate growth story as large technology companies continue to spend heavily on chips, cloud capacity and data centers.

Bitcoin, by contrast, is entering the second half of the year with weaker ETF flows, policy uncertainty and renewed questions about corporate treasury demand.

That divergence has left Bitcoin outside a rally in other high-growth assets. If AI continues to absorb capital through the summer, Bitcoin may need a stronger catalyst than lower prices to regain investor attention.

CLARITY Act becomes July’s policy catalyst

After a first half shaped by ETF outflows, renewed rate pressure and questions over corporate Bitcoin buyers, the Senate calendar has become one of crypto’s few near-term openings for a shift in sentiment.

The CLARITY Act would create a federal market structure framework for digital assets and define the roles of the Securities and Exchange Commission (SEC) and the Commodity Futures Trading Commission (CFTC).

Its passage would give exchanges, banks, asset managers and token issuers a clearer basis for building products and expanding services in the US.

A delay or failure would leave the industry facing the same regulatory uncertainty that has weighed on investment, product development and market confidence for years.

The timing is tight because US Senate leaders have only a narrow window before the August recess, while lawmakers still need to reconcile committee versions, address Democratic concerns over ethics and illicit-finance provisions, and secure enough votes to move the bill through the chamber.

That makes July a key test for the market. If the bill advances, Bitcoin could gain a policy catalyst at a time when ETF redemptions and macro conditions are weighing on risk appetite.

However, if the effort slips into the fall, one of the clearest sources of potential positive sentiment in the second half would fade.

In view of this, Thomas Perfumo, Kraken’s Chief Economist, described the CLARITY Act as the catalyst to watch over the next four weeks, saying passage could help restore sentiment and momentum.

Notably, Grayscale has also tied the bill to Bitcoin’s near-term path, placing it alongside Strategy’s balance-sheet decisions and the Fed’s rate outlook as factors that could determine whether BTC is nearing a low or remains exposed to further losses.